Living in the USA, we often think our homeowner's insurance policy has us covered for just about anything. But there's a crucial gap many overlook: flood damage. Most standard homeowner's policies explicitly exclude flood-related losses, leaving countless Americans financially vulnerable when disaster strikes. So, what exactly is flood insurance, and more importantly, do you need it in your area?

What is Flood Insurance & Why It's Different

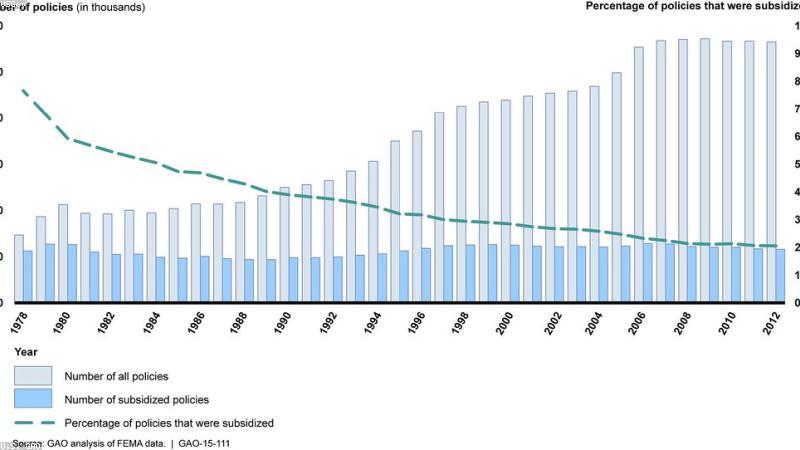

Unlike other perils like fire or theft, flood insurance typically isn't bundled with your standard homeowner's policy. It's a separate policy designed to protect your home and belongings from damage caused by flooding. The majority of flood insurance policies in the U.S. are provided through the National Flood Insurance Program (NFIP), managed by FEMA. However, a growing private flood insurance market also offers options, sometimes with broader coverage or lower premiums.

The distinction is vital: water damage from a burst pipe inside your home might be covered, but external water rising and inundating your property from a storm or overflowing river is almost certainly not by your standard policy.

Understanding Flood Zones: Do You Need Coverage?

The question of whether you "need" flood insurance often boils down to your property's location relative to FEMA's flood hazard maps. These maps designate areas into different flood zones based on risk levels:

- High-Risk Zones (e.g., A or V zones): If your property is in one of these zones and you have a mortgage from a federally regulated lender, flood insurance is typically mandatory. These areas have a 1% or greater annual chance of flooding (often called the 100-year flood plain).

- Moderate- to Low-Risk Zones (e.g., B, C, or X zones): While not mandatory, purchasing flood insurance in these zones is highly recommended. Statistics show that over 20% of all flood insurance claims come from properties outside high-risk areas. Remember, "low risk" doesn't mean "no risk." Heavy rainfall, unusual weather patterns, or development changes can quickly turn a dry area into a flood zone.

The truth is, anywhere it can rain, it can flood. Just a few inches of water can cause tens of thousands of dollars in damage to your home's structure and contents. Without flood insurance, these costs come directly out of your pocket.

Factors Influencing Flood Insurance Costs

Several factors determine your flood insurance premium, including:

- Your property's flood zone designation.

- The age and design of your home.

- Your home's elevation relative to the base flood elevation.

- The amount of coverage you choose for your building and contents.

- Your deductible.

NFIP policies have specific limits for building coverage (up to $250,000) and contents coverage (up to $100,000). Private options may offer higher limits.

The True Cost of Not Being Covered

Consider this: the average residential flood claim between 2016 and 2020 was nearly $52,000. For businesses, it's often far higher. FEMA disaster assistance, when available, typically comes in the form of low-interest loans, not free money, leaving you with debt to rebuild. Flood insurance, on the other hand, provides the funds directly to repair and replace your damaged property, without adding to your financial burden.

How to Determine Your Risk and Get Coverage

Don't wait until it's too late. Here's how to proceed:

- Check Your Flood Zone: Visit the FEMA Flood Map Service Center online to input your address and determine your property's current flood zone.

- Consult an Insurance Professional: An experienced agent specializing in flood insurance can help you understand your specific risks, explain NFIP and private market options, and provide tailored quotes.

Protecting your most valuable asset from flood damage is a critical step in comprehensive homeownership. Even if you're not in a "mandatory" zone, the peace of mind and financial security that flood insurance provides are invaluable. Act proactively to safeguard your home and future.